Fuel Excise Relief Is Not Disinflation

A temporary cut in fuel excise may reduce the pump price and trim headline CPI for a time, but it does little to relieve underlying inflationary pressure and may leave households worse off in the medium term.

A reduction in fuel excise has an obvious political appeal. Petrol prices rise, households notice the pressure immediately, and government lowers a visible tax. The arithmetic is simple, and the policy therefore appears simple. Yet the relevant economic question is not whether such a measure can lower the retail price of fuel for a period. It can. The relevant question is whether it addresses the inflation problem in any durable sense. In present circumstances, it does not. The current Commonwealth measure halves fuel excise for three months, reducing it by about 26.3 cents per litre, at an estimated budget cost of A$2.55 billion. That is substantial fiscal relief, but it is best understood as temporary price cushioning, not as a serious anti-inflation strategy.

The distinction between headline inflation and underlying inflation is central here. Headline inflation is the full CPI number, including volatile items such as fuel. Underlying inflation is what central banks watch more closely when they are trying to judge whether inflationary pressure is becoming persistent. A temporary fuel-tax cut can lower headline inflation because petrol is directly in the CPI basket. But that is not the same thing as reducing underlying inflation. It does not expand supply, lower imported fuel costs, or restore balance between aggregate demand and productive capacity. It changes one visible price for a time. The RBA’s February 2026 Statement on Monetary Policy made precisely this broader point: inflation had become more broad-based, capacity constraints were greater than previously assessed, and underlying inflation was higher than expected.

The 2022 episode illustrates the point clearly. The excise cut then was largely passed through to motorists. The ACCC found that wholesalers passed through the reduction in full and that, after six weeks, the cut had reached motorists in the vast majority of locations. The Parliamentary Budget Office also found that the temporary halving of excise lowered fuel prices by up to 24.3 cents per litre in the June quarter of 2022 and reduced CPI by around 0.6 percentage points, all else equal. But that same PBO analysis makes the larger point: when the excise rate returned to normal, the effect was unwound. The policy therefore did not solve inflation. It shifted the timing of one price effect and then reversed it.

The RBA’s own conduct in 2022 is more instructive than the temporary bowser relief itself. In May 2022, the Bank lifted the cash rate target to 0.35 per cent. By December 2022, it had raised the rate to 3.10 per cent. The reason is straightforward. The Bank did not interpret a temporary excise-related fall in petrol prices as evidence that inflation had been durably contained. It continued tightening because inflation remained too high and because returning inflation to target required a more sustainable balance between demand and supply. That is the correct lesson from 2022. A temporary tax reduction can coexist with continued monetary tightening because a lower pump price is not the same thing as disinflation.

The present environment makes that lesson more, not less, relevant. The ABS reported annual CPI inflation of 3.8 per cent in January 2026 and trimmed mean inflation of 3.4 per cent, both still above target-consistent levels. The RBA then raised the cash rate to 3.85 per cent on 3 February and to 4.10 per cent on 17 March. In its March statement, the Bank explicitly said that sharply higher fuel prices, if sustained, would add to inflation, that short-term inflation expectations had already risen, and that there was a material risk inflation would remain above target for longer than previously anticipated. This is the language of a central bank concerned about persistence, not one reassured by temporary retail relief.

Three simple figures help clarify the mechanism.

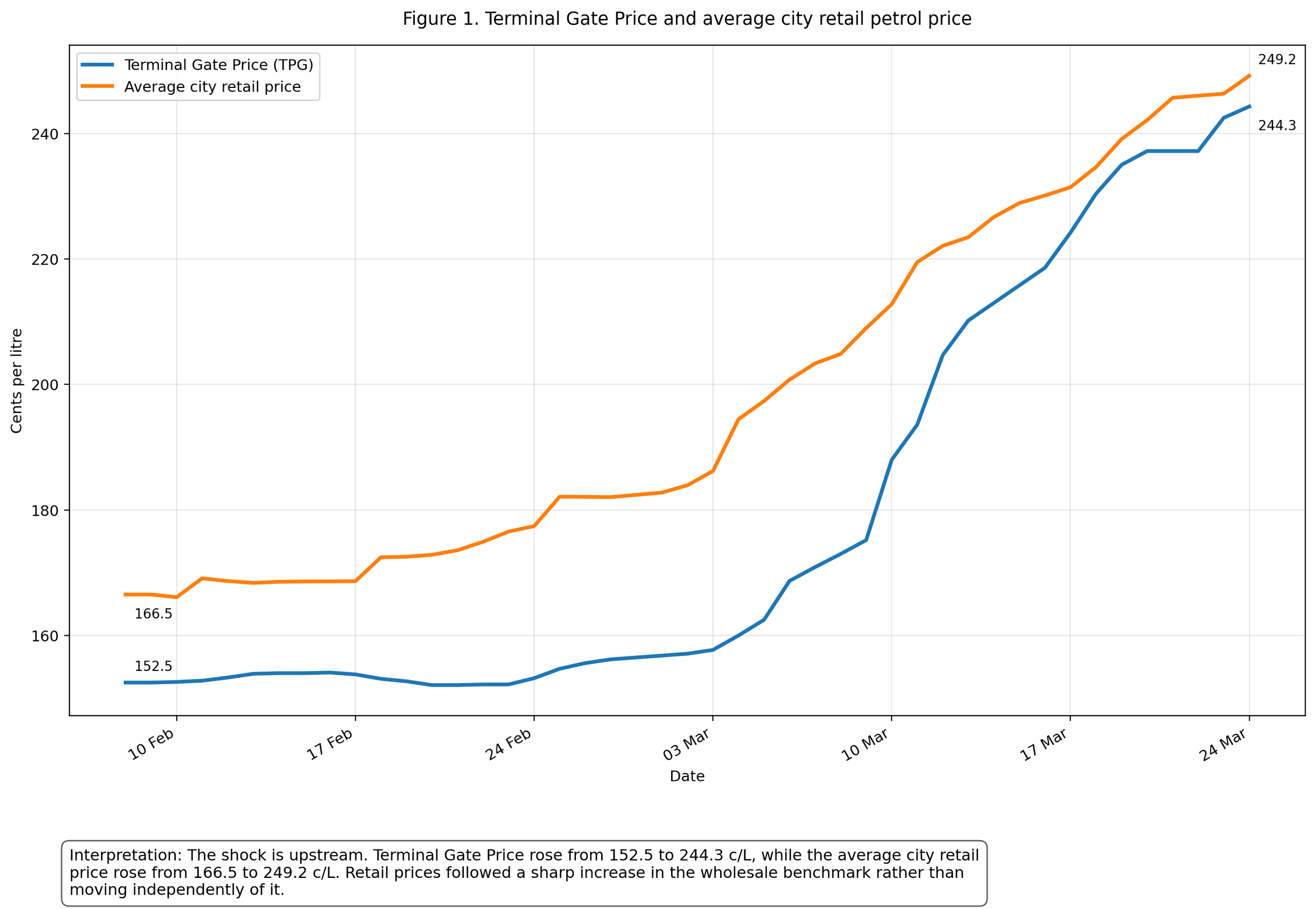

First, Terminal Gate Price versus average city retail price shows where the shock is located. Over the city-level daily series from 8 February to 24 March 2026, terminal gate price rises from 152.5 cents per litre to 244.3 cents, while the average city retail price rises from 166.5 cents to 249.2 cents. The wholesale benchmark rises first and more sharply.

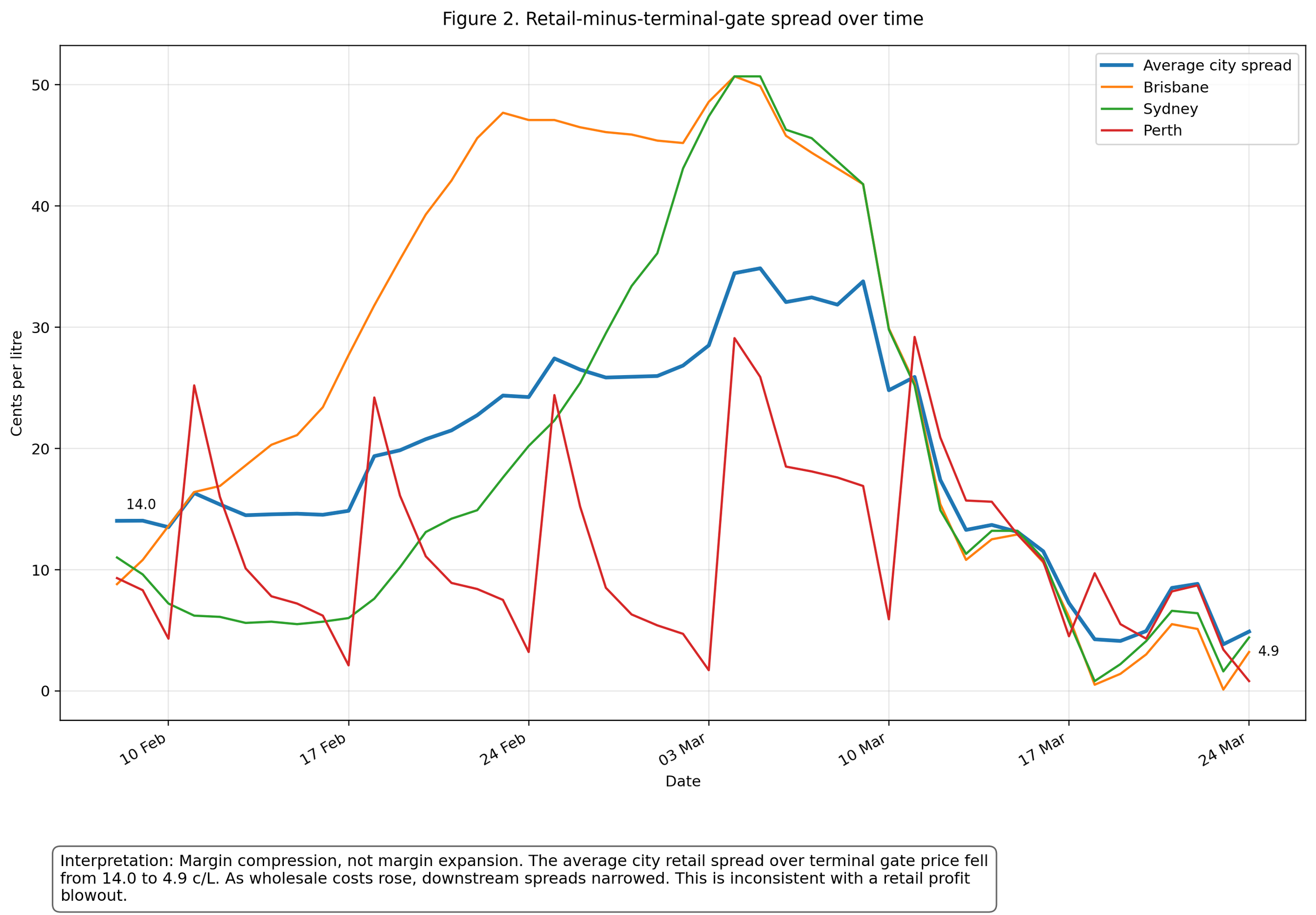

Second, retail minus terminal-gate spread over time shows whether the episode is better understood as a wholesale shock or a margin-expansion story. Over the same period, the average city spread falls from about 14.0 cents per litre to about 4.9 cents. Brisbane falls from 8.8 to 3.2 cents; Sydney from 11.0 to 4.4; Perth from 9.3 to 0.8. That is the critical chart because it indicates margin compression, not widening retail profit.

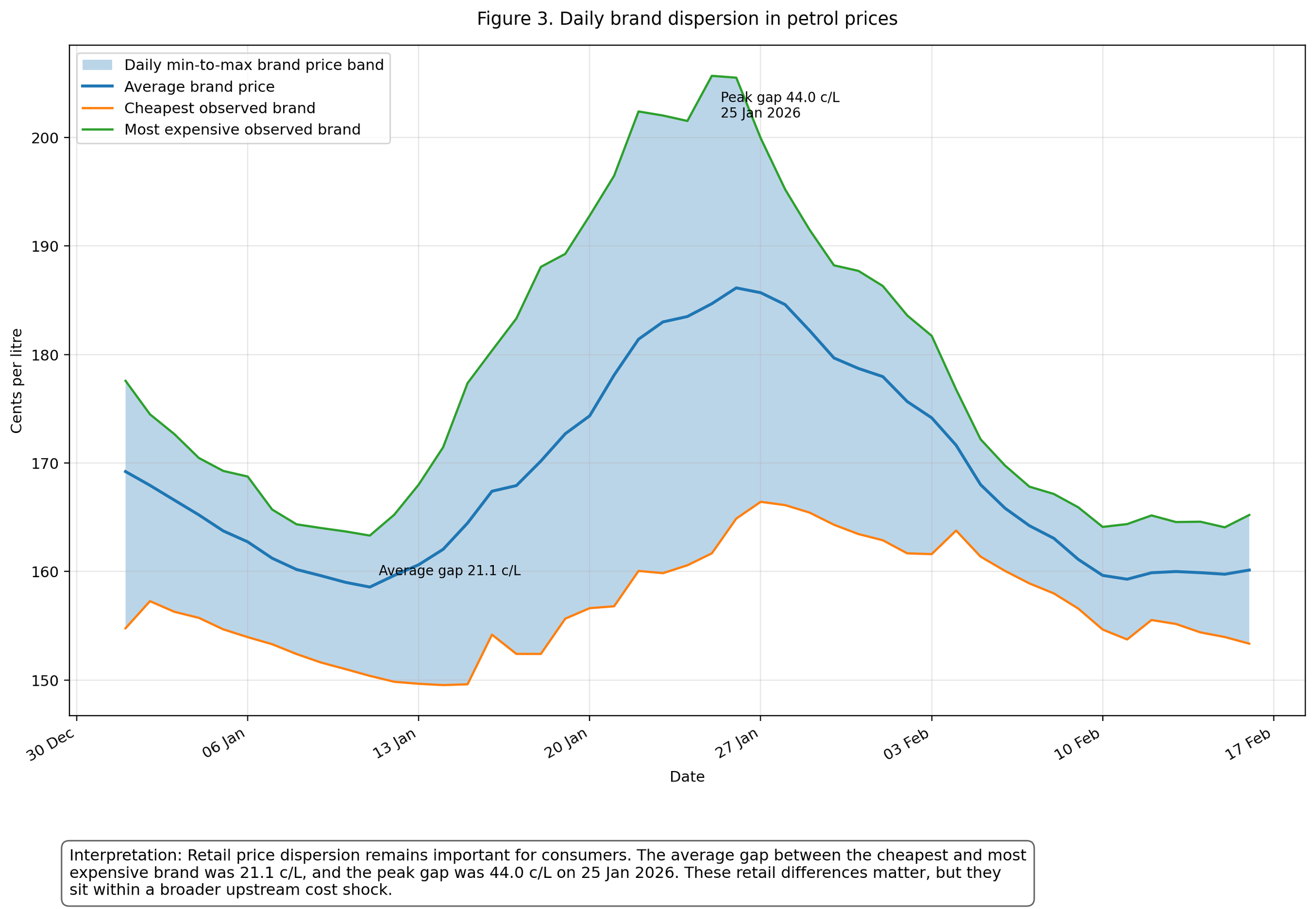

Third, brand dispersion by day, either as separate lines or as a min-to-max band, shows that retail competition still matters to consumers. Across the brand-level series, the average gap between the cheapest and most expensive brand is about 21.1 cents per litre, with a peak daily spread of about 44.0 cents. That matters for household shopping behaviour, but it does not alter the broader conclusion that the dominant present shock is upstream.

Once that is recognised, the policy limitation becomes clear. If the principal disturbance is an upstream cost shock, then a downstream tax cut cannot plausibly be described as a solution. It can moderate the final retail price for a time, but it does not lower crude prices, refined-product import prices, shipping costs, or geopolitical risk premia. Nor is it well targeted. A cents-per-litre subsidy delivers larger dollar gains to those who consume more fuel, not necessarily to those under the greatest financial strain. At the same time, it weakens the price signal that ordinarily encourages conservation when fuel is scarce or expensive. The result is a measure that is visible, immediate, and politically legible, but economically weak.

The medium-term household problem follows directly from this. Some families may save money at the bowser for a few months. But if underlying inflation remains elevated, the RBA is unlikely to treat that temporary relief as meaningful progress. Households then face the possibility of tighter monetary policy for longer, or at least a slower return to easier policy. Reuters reported on 31 March that markets were already pricing roughly a 60 per cent chance of another increase in May. Whether that occurs or not, the broader mechanism is the same: temporary petrol relief does not remove the forces that keep mortgage, rent and credit conditions under pressure.

That is why households can be worse off even when the policy appears helpful. They may receive a short-lived saving on fuel, but still face higher borrowing costs for longer, a weaker fiscal position, and a policy response that directs substantial public money toward a broad and poorly targeted subsidy rather than more durable or more selective relief. In that sense, fuel excise relief can be passed through to consumers and still constitute poor policy design. It lowers a visible price without resolving the inflation process that matters most.